What Does PAV Mean in Car Insurance? (Pre-Accident Value Explained)

Dealing with the aftermath of a car accident is stressful enough without having to decipher confusing insurance jargon. If you’ve recently lodged a claim, especially for a vehicle that might be deemed a “total loss” or write-off, your insurance adjuster has probably mentioned the acronym PAV.

You might be asking yourself: What does PAV mean in insurance, and why is the number they are offering me so low?

In this guide, the experts at OA Motor Assessing explain exactly what the Pre-Accident Value meaning is, how insurers calculate it, and—most importantly—what you can do if you believe your insurer is trying to shortchange you.

The Definition: What is PAV in Insurance?

PAV stands for Pre-Accident Value.

In the motor insurance industry, the Pre-Accident Value is the exact, fair market value of your vehicle immediately before the accident occurred.

Think of it this way: If you had parked your car on the side of the road with a “For Sale” sign in the window five minutes before the crash, the PAV is the realistic price a willing buyer would have paid you for it.

Why is PAV so important?

If your insurance policy covers your car for “Market Value” (rather than an “Agreed Value”), the PAV is the maximum amount of money your insurance company will pay you if your car is written off.

How Do Insurance Companies Calculate Your PAV?

When an insurance assessor determines the PAV of your vehicle, they rarely inspect your specific car’s unique history and condition. Instead, they rely heavily on automated computer systems and generic industry pricing guides (like Redbook or Glass’s Guide).

They input basic data points into their system:

- Make and Model

- Year of manufacture

- General odometer reading

- Standard factory features

While this “cookie-cutter” approach is fast and cost-effective for the insurance company, it is very often highly inaccurate for the car owner.

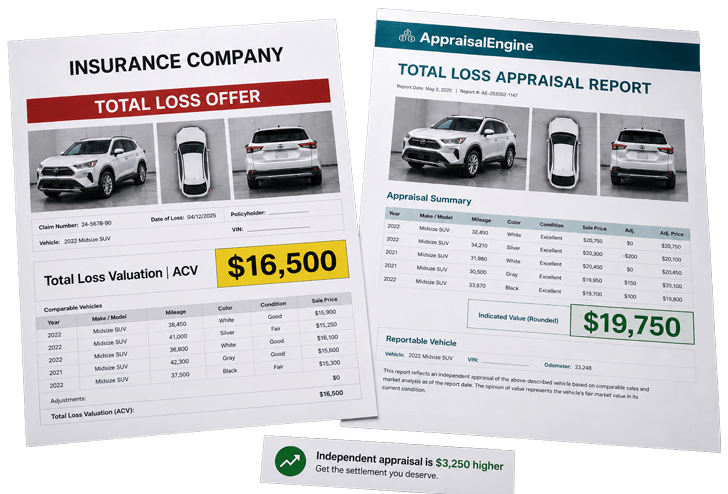

The Problem: Why Your Insurer’s PAV Offer is Probably Too Low

The biggest flaw in the insurance company’s method is that they treat every 2016 Ford Ranger or 2018 Toyota Corolla as if they are exactly the same. But as a car owner, you know that isn’t true.

Generic online calculators and insurance algorithms routinely fail to account for the things that make your specific vehicle more valuable, such as:

- Exceptional Condition: A car that has been meticulously garaged, detailed regularly, and has perfect paintwork is worth more than a fleet vehicle with sun damage and scratches.

- Aftermarket Accessories: Insurers often ignore thousands of dollars spent on bull bars, custom canopies, upgraded suspension, specialized wheels, or high-end sound systems.

- Extremely Low Kilometers: If your car has been driven far less than the national average, its market value is significantly higher.

- Recent Major Upgrades: Brand new tires, a recently rebuilt transmission, or a newly replaced engine right before the crash add undeniable value to the vehicle.

- Local Market Scarcity: Used car prices fluctuate. If your specific model is currently in very high demand but low supply in your area, the generic pricing guides insurers use are often months out of date.

Do I Have to Accept the Insurance Company’s PAV?

Absolutely not. This is the most common misconception among drivers.

An insurance company’s first offer is just that—an offer. It is an opening negotiation. If you believe the Pre-Accident Value they have placed on your car is too low and does not reflect its true market worth, you have the legal right to dispute it.

However, you cannot just tell the insurance company you want more money. You must provide them with concrete, professional evidence.

How to Fight a Low PAV Offer and Win

To successfully dispute an insurer’s valuation, you need an Independent Pre-Accident Valuation report.

This is where OA Motor Assessing steps in. As independent, qualified motor vehicle assessors, we don’t rely on generic algorithms. We work for you, not the insurance company.

When you hire us to assess your vehicle, we manually investigate:

- The exact condition of your car prior to the crash.

- Every single accessory and modification you have added.

- Your service history and recent mechanical investments.

- Real-time, current market data for comparable vehicles in your specific region.

We compile this data into a legally sound, comprehensive valuation report. When you hand an OA Motor Assessing report to your insurance company, it forces them to look past their automated systems and pay you the true, fair market value for your vehicle.

Don’t let the insurance company dictate what your car was worth.

If you are facing a write-off and want to ensure you aren’t left out of pocket, (Note: Hyperlink this bracketed text directly to your service URL: https://oa.business/motor-vehicle-assessing/pre-accident-valuation/ )

{kind=link}

{kind=link}

{kind=link}

{kind=link}