What happens if insurance writes off my car?

Getting into a car accident or having your vehicle severely damaged by hail, flood, or fire is stressful enough. But when your insurance company calls to deliver the news that your car is a “total loss”—otherwise known as a write-off—the confusion and anxiety can quickly escalate.

What exactly does a write-off mean? How is your payout calculated? Can you keep the car? And most importantly, what if the insurer’s payout offer is thousands of dollars below what it would actually cost to replace your car in today’s market?

In this comprehensive guide, OA Motor Assessing breaks down the Australian insurance write-off process, explains your legal rights, and outlines how an independent vehicle assessment can protect you from being shortchanged by your insurer.

1. What Does “Write-Off” Actually Mean in Australia?

In Australia, a vehicle is declared a write-off (or total loss) when an insurer determines that it is either unsafe to repair or that the cost of repairing it is uneconomical.

When this happens, the insurer will take ownership of the vehicle, cancel your policy, and pay you out according to the terms of your Product Disclosure Statement (PDS).

There are two distinct categories of write-offs under Australian road transport regulations:

Category A: Statutory Write-Off

A statutory write-off is a vehicle that has suffered severe structural, water, or fire damage. It is deemed completely unsafe to ever be repaired and returned to Australian roads.

What happens to it: The vehicle’s Vehicle Identification Number (VIN) is permanently recorded on the national Written-Off Vehicle Register (WOVR). The car can only be sold for scrap metal or dismantled for individual spare parts. It can never be re-registered.

Category B: Repairable Write-Off

A repairable write-off is a vehicle that has suffered damage that could technically be repaired, but the insurer has decided that the total cost of repairs plus the salvage value of the wreck exceeds the vehicle’s pre-accident value.

What happens to it: This is where state-based laws differ significantly:

New South Wales (NSW): Under strict NSW laws, almost all light vehicles written off are classified as statutory write-offs and cannot be re-registered, even if they are technically repairable. This is to deter vehicle rebirthing and protect buyers from unsafe vehicles.

Victoria, Queensland, Western Australia, South Australia, and other territories: In these states, a repairable write-off can be bought back (usually by the owner or a licensed repairer), fully repaired to manufacturer standards, and re-registered. However, it must first pass a highly rigorous identity and safety inspection (such as a Vehicle Identity Validation [VIV] test in Victoria or a Written-Off Vehicle Inspection [WOVI] in Queensland).

2. How is Your Write-Off Payout Calculated?

Many policyholders expect to receive a cheque for the full amount their car was insured for. However, the final payout calculation involves several factors, and the final figure is often lower than anticipated.

Your payout is determined by whether you have Agreed Value or Market Value coverage:

Agreed Value vs. Market Value

Agreed Value: You and your insurer agreed on a fixed dollar amount for the vehicle when you took out or renewed your policy. If your car is written off, this is the base figure the insurer starts with.

Market Value: The insurer calculates the cost to replace your vehicle with an identical one of the same make, model, age, mileage, and condition in your local market immediately prior to the accident.

The Market Value Trap: Insurers rarely do manual, localized research for your specific vehicle. Instead, they use automated databases (like RedBook or Glass’s Guide) that default to the lowest average market price. This often completely ignores factors like immaculate pre-accident condition, low kilometres, regional price inflation, or hard-to-find vehicle variants.

Deductions from Your Payout

Once the base value (Agreed or Market) is established, insurers will make several deductions before sending you the final payment:

Your Excess: Any applicable policy excesses (basic, age, or unlisted driver excesses) will be deducted if you were at fault or if you cannot identify the third party at fault.

Remaining Insurance Premiums: If you pay your insurance premium monthly rather than annually, the insurer will deduct the remaining monthly instalments for the rest of your policy year. This is because a total loss claim “fulfils” the contract, and the policy is cancelled.

Unused Registration and CTP: Depending on your state and insurer, the registration and Compulsory Third Party (CTP) insurance may be cancelled, and the refund amount might be deducted or kept by the insurer as salvage rights.

3. What Happens If You Want to Keep the Car?

If your car is declared a repairable write-off and you have a sentimental attachment to it (or believe you can repair it cheaper yourself), you do have the right to ask your insurer if you can keep the vehicle. This is known as keeping the salvage.

If the insurer agrees:

They will calculate the salvage value of the wreck (what they would have received for it at a salvage auction, usually 10% to 30% of its pre-accident value).

They will deduct this salvage value, along with your excess, from your final payout.

You keep the damaged car and the remaining cash payout.

Important: You will be responsible for transporting the wreck, repairing it to professional standards, and paying for the costly state-based roadworthy and WOVR inspections to get it re-registered.

4. Unhappy with Your Payout Offer? Your Rights and Steps to Dispute

It is incredibly common for car owners to receive an initial payout offer from their insurance company that is thousands of dollars below what it would actually cost to buy a replacement vehicle.

Remember: You do not have to accept the insurer’s first offer.

Insurance companies are commercial entities looking to minimize their payouts. You have clear legal rights under the General Insurance Code of Practice to dispute their valuation. Here is the step-by-step process to challenge a lowball payout offer:

Step 1: Do Not Accept or Sign Anything

Once you accept a payout offer, sign the discharge authority, or cash the insurer’s cheque, you have legally settled the claim. It is extremely difficult to reopen a claim once it is finalized. Politely tell your claims handler that you reject the offer and will be gathering evidence to dispute the valuation.

Step 2: Request the Insurer’s Valuation Report

Ask your insurer to provide the written valuation report they used to calculate your vehicle’s market value. Check this document thoroughly for errors. Insurers often list the wrong trim level, miss factory-fitted options, overestimate the vehicle’s mileage, or compare your car to lower-spec models or vehicles located interstate in cheaper markets.

Step 3: Gather Local Market Evidence

Go online to platforms like Carsales.com.au, Autotrader, and Facebook Marketplace. Find advertisements for vehicles of the exact same make, model, year, and trim level, with similar kilometres, located in your home state. Print or screenshot these listings to show what it actually costs to buy a replacement car today.

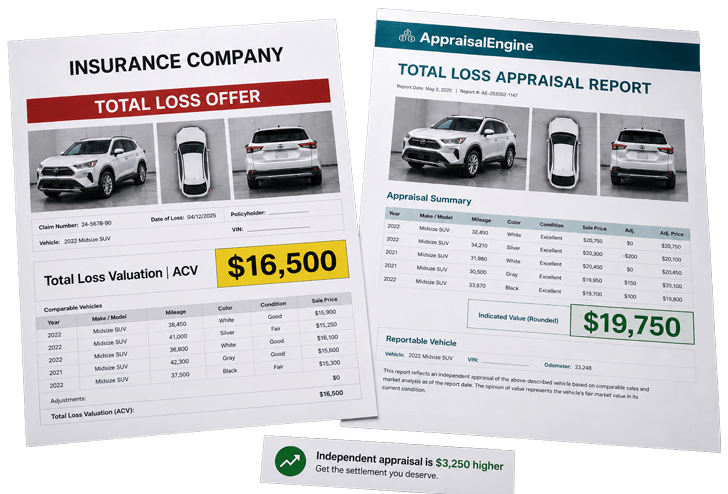

Step 4: Obtain an Independent Motor Vehicle Assessment (The Key to Success)

This is where many disputes are won. Insurers will often dismiss screenshots from car sales websites as “asking prices, not selling prices.” However, they cannot dismiss an Independent Valuation Report from a qualified, licensed motor vehicle loss assessor.

An independent assessor, such as OA Motor Assessing, will conduct a comprehensive, professional valuation of your vehicle. This includes:

Analysing pre-accident photos of your car to document its pristine condition.

Reviewing your service history and mechanical receipts (proving your car was meticulously maintained).

Evaluating any declared modifications or high-value aftermarket additions (e.g., bull bars, heavy-duty suspension, custom trays, or high-end sound systems).

Compiling a comprehensive local market analysis using real-world transaction data, not just automated database averages.

Our independent reports are legally structured, professional documents designed to comply with the guidelines set by the Australian Financial Complaints Authority (AFCA).

Step 5: Lodge a Formal Internal Dispute

Submit your independent valuation report and supporting evidence to your insurer’s Internal Dispute Resolution (IDR) department. By law, Australian insurers must have an IDR process. Under the General Insurance Code of Practice, they are required to review your dispute and provide a formal response, usually within 30 days.

Step 6: Escalate to AFCA (If Required)

If the insurer’s IDR department still refuses to offer a fair payout, you can escalate your complaint to the Australian Financial Complaints Authority (AFCA).

AFCA is a free, independent dispute resolution scheme for consumers.

Once a complaint is lodged with AFCA, the insurer is blocked from finalizing your claim or forcing a low settlement.

AFCA heavily relies on professional, independent evidence. Having an OA Motor Assessing report is often the deciding factor that forces insurers to settle for the higher, correct amount before AFCA even reaches a formal determination.

5. What Can an Independent Assessment Save or Gain You?

Engaging an independent assessor like OA Motor Assessing requires a small upfront fee, but the return on investment can be substantial.

In many cases, an independent valuation can increase your insurance payout by $3,000 to over $15,000, depending on your vehicle type and pre-accident condition.

Here are the specific scenarios where an independent assessment has the highest chance of gaining you a significantly higher payout:

| Scenario | Why the Insurer Lowballs You | How OA Motor Assessing Solves It | Potential Payout Gain |

| Low-Kilometre Vehicles | Insurer databases default to “average” kilometres for the car’s age (e.g., assuming a 10-year-old car has done 150,000km). | We document and prove your car only had 40,000km, which carries a massive premium in the real-world Australian market. | $3,000 – $8,000+ |

| Immaculate / Enthusiast Cars | Insurers treat a pristine, enthusiast-owned car the same as a neglected, dented daily driver of the same year. | We present evidence of the vehicle’s pristine paintwork, immaculate interior, and complete logbook service history. | $4,000 – $12,000+ |

| Modified 4WDs & Utilities | Insurers often ignore aftermarket accessories like bull bars, winches, snorkels, canopies, and suspension upgrades. | We calculate the depreciated replacement value of all declared, high-value modifications and add them to the pre-accident vehicle value. | $5,000 – $15,000+ |

| Classic, Rare, or Imported Vehicles | Standard Australian insurer databases do not have accurate pricing data for classic cars, rare trims, or grey imports. | We conduct specialist market research, sourcing sales data from specialist auctions, classic car clubs, and historical sales trends. | $10,000 – $25,000+ |

| Recent Major Maintenance | Insurers do not account for a brand-new transmission, fresh set of premium tyres, or major engine rebuild completed just weeks before the accident. | We prove that these major mechanical works increased the immediate pre-accident market value of the vehicle. | $2,000 – $5,000+ |

Take Control of Your Insurance Write-Off Claim Today

Your insurance policy is a legal contract designed to restore you to the financial position you were in immediately before the accident—no more, no less. If your insurer’s payout offer doesn’t allow you to buy an equivalent replacement vehicle in the current Australian market, they are failing to meet their contractual obligation.

Don’t let a major corporate insurer dictate the value of your asset. Protect your financial interests with a professional, legally binding independent valuation.

Contact OA Motor Assessing today for an obligation-free chat about your write-off dispute. Let our expert independent motor assessors help you secure the fair, honest payout you deserve.

Disclaimer: This article is for informational purposes only and does not constitute formal legal or financial advice. If you are disputing an insurance claim, please consult with a qualified professional or contact AFCA directly for guidance based on your specific circumstances.

{kind=link}

{kind=link}

{kind=link}