Do I Have to Accept My Car Insurance Payout Offer? (Your Rights Explained)

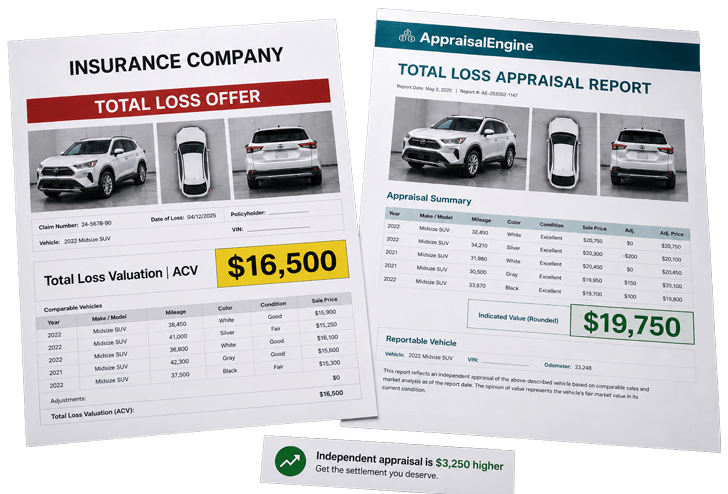

Getting the news that your car is a “total loss” or a write-off is a stressful experience. But for many Australian drivers, the real shock comes a few days later when the insurance company officially emails through their settlement offer.

You look at the payout figure, look at the current prices of cars for sale online, and realize a harsh truth: This money won’t even come close to replacing my car.

This leads to the most common question we hear from frustrated drivers at OA Motor Assessing: Do I have to accept the insurance company’s payout offer?

Here is everything you need to know about your rights, why their offer is probably too low, and exactly how you can fight back.

The Short Answer: No, You Do Not Have to Accept

The direct answer is no. You are under absolutely no legal obligation to accept the first settlement offer your insurance company presents to you.

An initial payout figure is simply the insurance company’s opening offer. Under Australian law and the General Insurance Code of Practice, if you believe their Pre-Accident Value (PAV) calculation is inaccurate, you have the right to reject the offer and lodge an official dispute.

Your insurance company cannot force you to sign the settlement, nor can they cancel your valid claim simply because you disagree with their valuation.

Why is the Insurance Company’s Offer So Low?

To understand how to fight the offer, you need to understand how the insurer calculated it in the first place.

Insurance companies process thousands of total loss claims every single week. To save time and money, they do not send a human being to thoroughly inspect the unique history of your car. Instead, they use automated computer software and generic industry pricing guides (like Glass’s Guide or Redbook).

These calculators generate the value of an “average” vehicle of your make and model. However, your car likely isn’t average.

Automated insurance calculators routinely ignore:

Thousands of dollars in aftermarket accessories: (e.g., custom canopies, bull bars, upgraded suspension, or specialized wheels).

Exceptional pre-crash condition: (e.g., a car that was meticulously garaged and detailed vs. one left in the sun).

Recent major mechanical upgrades: (e.g., a brand new transmission or heavy-duty clutch installed weeks before the crash).

Real-time market scarcity: Automated guides lag months behind the real Australian used-car market. If your specific vehicle type is currently in high demand, the insurer’s guide won’t reflect it.

Your Rights: The Dispute Process in Australia

If you reject the offer, you are entering a dispute. Here is how the process works and the rights you hold:

Internal Dispute Resolution (IDR): You have the right to challenge the valuation through your insurer’s IDR team. You must present evidence as to why their number is wrong.

The Right to Request Their Data: You have the right to ask your insurance adjuster exactly how they arrived at their figure. Ask them for the valuation report they used.

External Escalation (AFCA): If the IDR team still refuses to offer a fair true market value, you have the right to escalate your complaint to the Australian Financial Complaints Authority (AFCA) for an independent legal ruling.

How to Successfully Dispute the Offer (Your Action Plan)

It is vital to understand that you cannot simply call your insurer, say “I want more money,” and expect them to pay up. Sending them screenshots of expensive cars on Carsales.com.au also won’t work, as asking prices are not guaranteed sales prices.

To win a dispute, you must provide Expert Evidence.

Here is your action plan:

Step 1: Do Not Sign Anything. If you sign the settlement release form or agree to the payout over the phone, the claim is closed. Do not accept the funds if you plan to dispute.

Step 2: Tell them you are disputing the PAV. Politely inform your adjuster in writing that you reject the offer and will be obtaining your own independent valuation.

Step 3: Get an Independent Total Loss Assessment. This is your ultimate weapon. You need to hire a licensed, independent motor vehicle assessor.

Why You Need an Independent Assessor

Unlike the insurance company’s computer algorithm, an independent assessor works exclusively for you.

At OA Motor Assessing, our experts manually investigate the exact reality of your vehicle. We physically itemize your modifications, review your mechanical receipts, verify your logbooks, and cross-reference this with real-time, local market sales data.

We compile this into a legally robust, comprehensive True Market Value Report. When you hand an OA Motor Assessing report to your insurer (or to AFCA), it forces them to stop looking at their automated generic calculators and start looking at the undeniable facts of your specific vehicle.

Don’t leave thousands of dollars on the table just because fighting the insurer feels intimidating.

If you are holding a lowball settlement offer and want to demand your car’s true worth, we can help. Click here

: https://oa.business/motor-vehicle-assessing/total-loss-dispute-assessment/ )

{kind=link}

{kind=link}

{kind=link}